Documentation Index

Fetch the complete documentation index at: https://docs.synctera.com/llms.txt

Use this file to discover all available pages before exploring further.

ACH Procedure

ODFI (Originating Depository Financial Institution)

- The Synctera platform creates ACH NACHA formatted files for exchange with the Fed (.ach formatted) with entries originated by the Originator

- Synctera follows the NACHA rules and restricts origination to WEB and CCD SEC codes. Originators can originate CREDIT and DEBIT entries after a successful receiver’s account verification process

- Originator’s customer and businesses go through a KYC and KYB process before being able to originate entries

- Originator’s customer and business are periodically screened for OFAC in the Synctera platform

- Receiver’s account or external accounts are verified via Plaid or Microdeposits

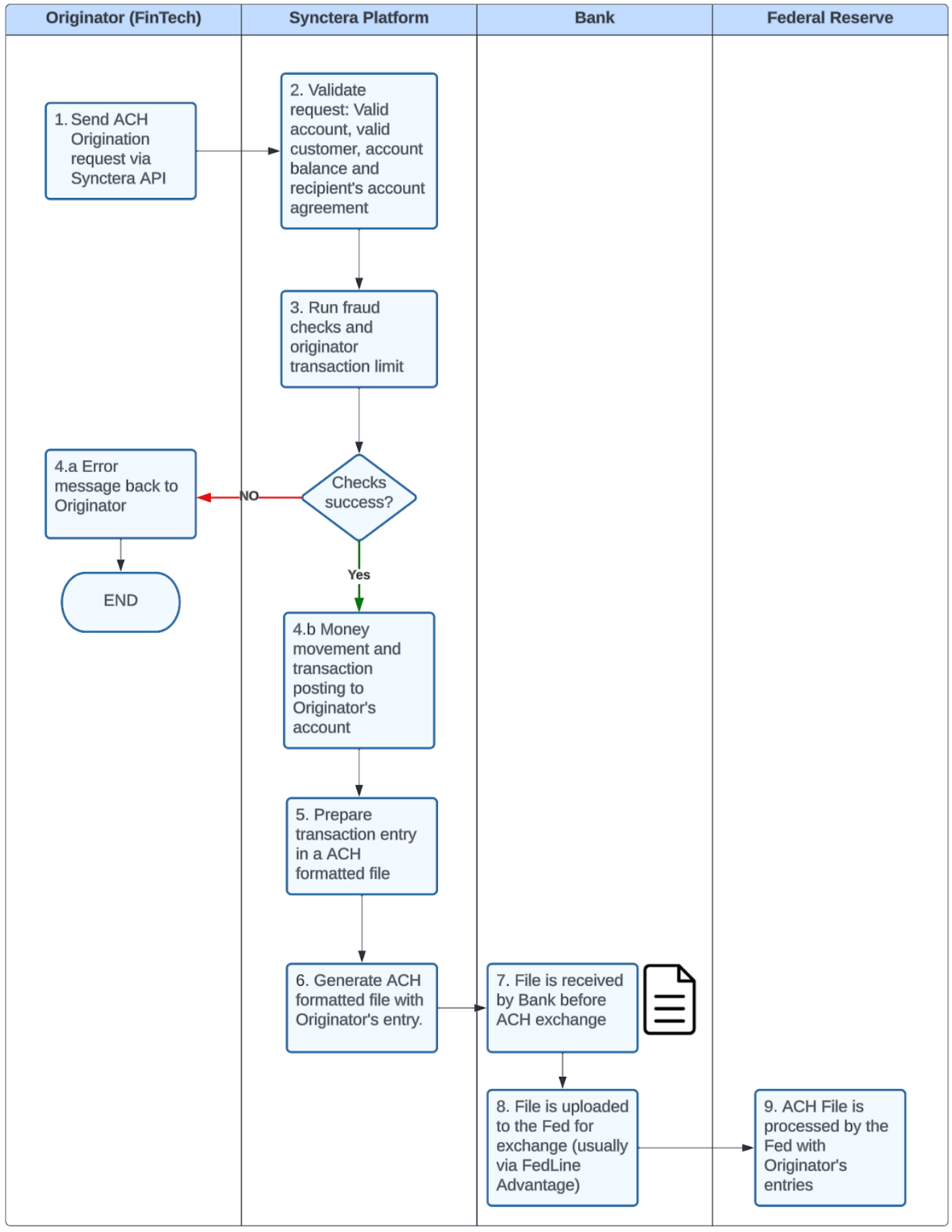

High level ACH Origination flow:

ACH Origination Prerequisites:

- In order to originate ACH DEBITS or CREDITS in the Synctera platform Originator’s customer or the business need to be KYC’d and/or KYB’d

- The Originator’s business or the customer needs to have a valid account in status ‘ACTIVE’ and ACH Origination needs to be enabled for that account

- In order to originate ACH DEBITS for consumers the FinTech customer must link the receiver’s account via Plaid using their banking credentials or if approved by the Bank to provide a proof of external account ownership i.e a void check

- For business customers, In order to originate ACH DEBITS and CREDITS to a different party they can only originate after obtaining an explicit ACH DEBIT Authorization from the receiver.

- The Originator requests the ACH Origination to the Synctera platform via API

- Originators can initiate Same day ACH entries and Non-same day entries through the Synctera platform. A same day / non same day option is provided to the Originator.

- The Synctera platform keeps track of the Fed working days to generate ACH files. ACH files only originated on business days.

Verify Originator’s customers:

The FinTech adheres to Customer Identification Program (CIP) and customer due diligence guidelines to incorporate regulatory guidance and requirements along with industry proven practices for all new customers. These practices incorporate risk rating tools to identify and mitigate new account risk, maintain a quality customer base, and to confirm risks are within acceptable risk tolerance guidelines as they relate to the creditworthiness of the customer.

Proof of authorization:

FinTech is responsible for obtaining and storing the ACH Credit or Debit proof of authorization from its customers.

The FinTech will complete an annual audit of its compliance with the Nacha Rules and other applicable laws by December 31st of each year. The scope of the audit includes data and network security, record retention, agreements and authorizations, system access controls, and any additional areas required by the Bank.

Transaction validation and limit checks:

The Synctera platform runs a set of transaction validations each time the FinTech wants to initiate the origination of an ACH Debit or ACH Credit. The transaction validations are the following and are not performed in this specific order:

Originator account status and customer status: The Synctera platform checks the originator account status, the account needs to be active to initiate an ACH. Additionally we perform checks on the customer status or business status, only customers and/or businesses with a successful KYC or KYB can initiate ACH transactions.

Originator transaction limit: As part of the FinTech Onboarding process, the bank and the Originator agree on a set of transaction limits, per transaction, per customer as an Originator overall. The Synctera platform checks the different limits at the time of transaction origination and determines whether that transaction can be originated within the limits or is declined due to exceeding the limits.

Originator account-specific limits: Additionally to the Bank and Originator agreed limits, The FinTech can decide to establish account specific limits for its customers that should be always lower than the ones agreed in between the originator and the Bank.

The Synctera platform checks the account-specific limits at the time of origination, if failed, the Originator receives a decline.

Receivers account validation (external account): In order to initiate ACH transfers the Originator needs to link the receiver’s external account via Plaid or Microdeposits, this validation is required for Originators that want to initiate ACH Debits.

For ACH Credits the Originator needs to store the receiver’s account information in the Synctera platform.

When the FinTech initiates the ACH Origination request, the Synctera platform validates that the Receiver’s account is validated and is an active account.

Account balance validation and transaction funding: When the FinTech customer requests an ACH Origination (Credit or Debit) the Synctera platform will perform an account balance check against the account initiating the transfer.

In the case of an ACH CREDIT (push funds) transfer, the funds will be moved out of the Customer account to secure the transfer funds, following the transaction pre-funding model.

In the case of an ACH DEBIT (pull funds) the funds will be credited to the FinTech customer account in real time but a hold of funds will be set for two business days. The hold of funds helps to prevent account overdrafts for most common inbound ACH returns.

ACH transaction effective date (applicable for future-dated ACH origination): Originators can request the creation of outbound ACH Credits or Debits with effective dates in the future. The Synctera platform validates that the ACH transfers can only be originated up to two business days in advance. Business days for ACH transactions are dictated by the Fed calendar.

Additional checks: At the time of ACH file creation and before sending the file to the bank, the Synctera platform checks again the Originator customer or business KYC/KYB status and the account status to make sure the status has not changed in between the FinTech requesting the payment origination (for example on a Saturday) and the payment being sent to the Bank (on the following business day) if any of the statuses have changed then the payment will be canceled and not included in the file to be sent to the Fed.

Transaction fraud checks: The Synctera platform performs fraud checks using a fraus Engine. The fraud Engine used by the Synctera platform is Feedzai. Fraud rules are reviewed in detailed with the Bank at the time of FinTech Onboarding

ACH CREDIT (Push) Origination:

FinTechs can originate ACH Credits against receivers accounts (external accounts). When a FinTech initiates an ACH Credit and passes all checks and validations, the Originator’s account is debited in real time and funds are credited to an internal ACH Settlement account, therefore funds are guaranteed.

If the FinTech originates a future-dated ACH Credit, the funds will be debited in real time as well and sent to the Bank in the next available exchange with its effective date in the future. FinTechs can originate future-dated entries up to two business days in advance and as per NACHA rules future dated transactions can be sent as part of the same-day origination windows.

ACH DEBIT (Pull) Origination:

FinTechs can originator ACH Debits (Pulls) to verified receiver’s accounts. The Synctera platform will credit the Originator’s account in real time and set a hold of funds for two business days.

The intent of the hold of funds is to guarantee funds and reduce the account overdraft risk in the event of a return, most returns are received within two business days of the file exchange.

Originators and banks can negotiate the length of the hold of funds as part of their agreements.

If the FinTech originates a future-dated ACH Debit, the funds will be credited in real time and a hold of funds is placed for two business days from the payment effective. The payment effective date in this scenario is in the future (i.e if a FinTech originates an ACH Debit on a Tuesday, effective on Thursday the hold of funds will be active until Monday).

The ACH Debit entry is sent to the Bank in the next available exchange with its effective date in the future. FinTechs can originate future-dated entries up to two business days in advance and as per NACHA rules future dated transactions can be sent as part of the same-day origination windows.

ACH RETURN Origination and return rate tracking:

The Synctera platform originates ACH Returns on FinTech’s behalf in response to the Inbound ACH file processing as the RDFI.

ACH Outbound returns are created when the Inbound ACH file is processed. The Synctera platform will create returns following the NACHA rules and within the NACHA rules timeframes.

The Synctera platform provides return reporting for Banks to oversee the returns generated for their ABA number broken down by FinTech.

The reporting is aligned to the NACHA specifications.

ACH REVERSAL Origination:

The Synctera platform has appropriate controls to make sure that it doesn’t generate duplicate files. In the event where a duplicate file is created, the platform can originate file reversals for a duplicate file or for an erroneous file in compliance with the NACHA requirements.

The Bank is informed of the duplicate file creation.

ACH Disputes Origination:

The Originator’s customers can initiate ACH Disputes for an Inbound ACH Credit or ACH Debit originated from an external FI. The FinTech needs to collect the dispute information and proof from their customer and after the Synctera compliance operations team reviews it and considers it a valid dispute, then the Dispute will be initiated with the network.

Synctera cannot dispute entries in the ACH network when the original entry is originated by the Synctera platform. In this scenario the Originator can request the RDFI to return the entry.

ACH Settlement with the Fed:

The Bank is responsible to settle funds with the Fed as the ODFI for originated entries by their Originators (FinTechs).

The Settlement will be performed by the Fed based on the entry effective date.

The Settlement instructions are provided by the Bank to the Fed when the ABA number is onboarded for ACH processing with the Fed.

The Bank uses the FinTech FBO to fund the settlement for debit positions and when the settlement is a credit position funds are moved to the FinTech FBO

File exchange:

The Synctera platform is configured to participate in the three same-day file exchanges with the Fed and the exchange times with the bank can be configured to the banks timezone