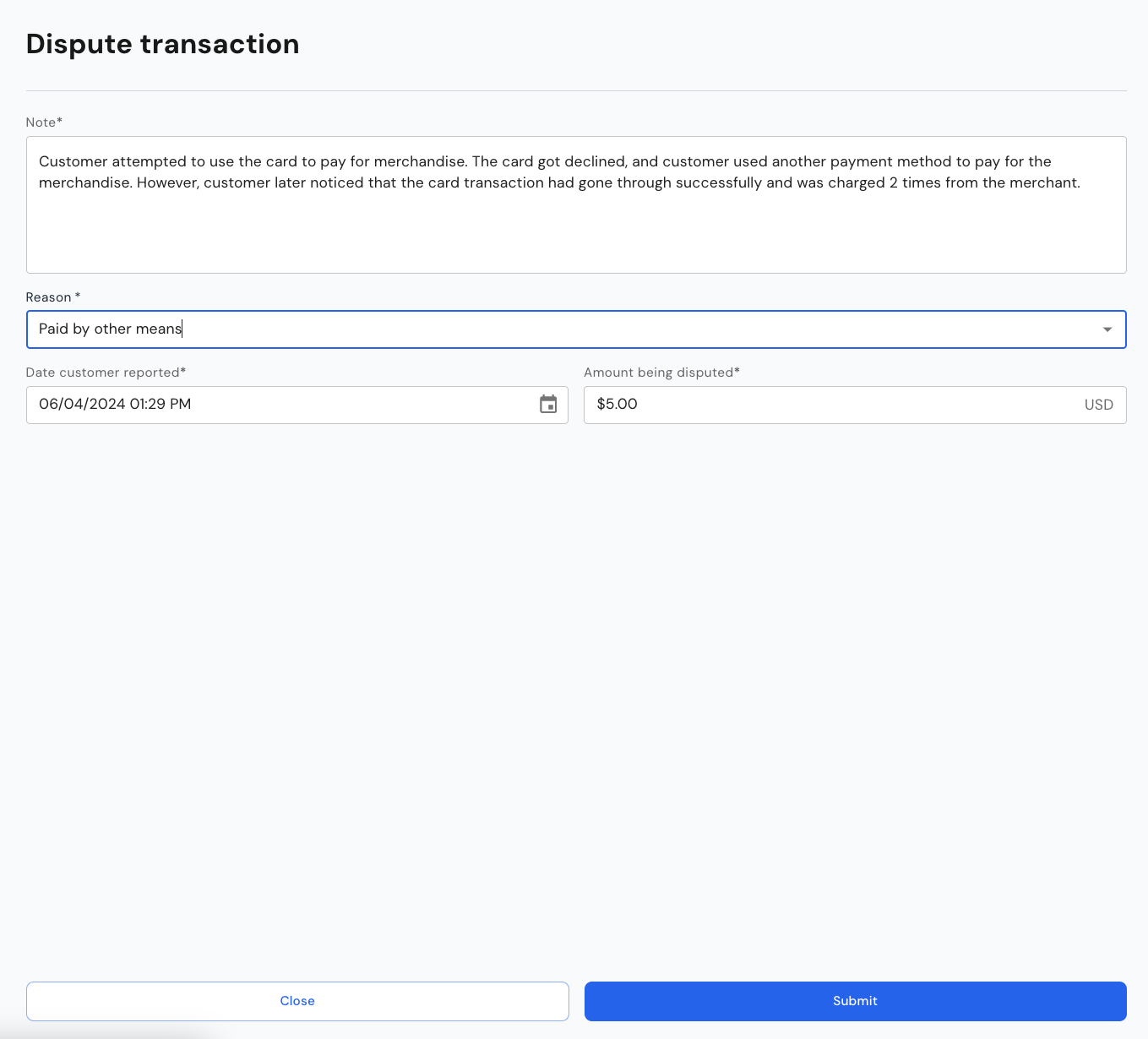

How to submit a card transaction dispute?

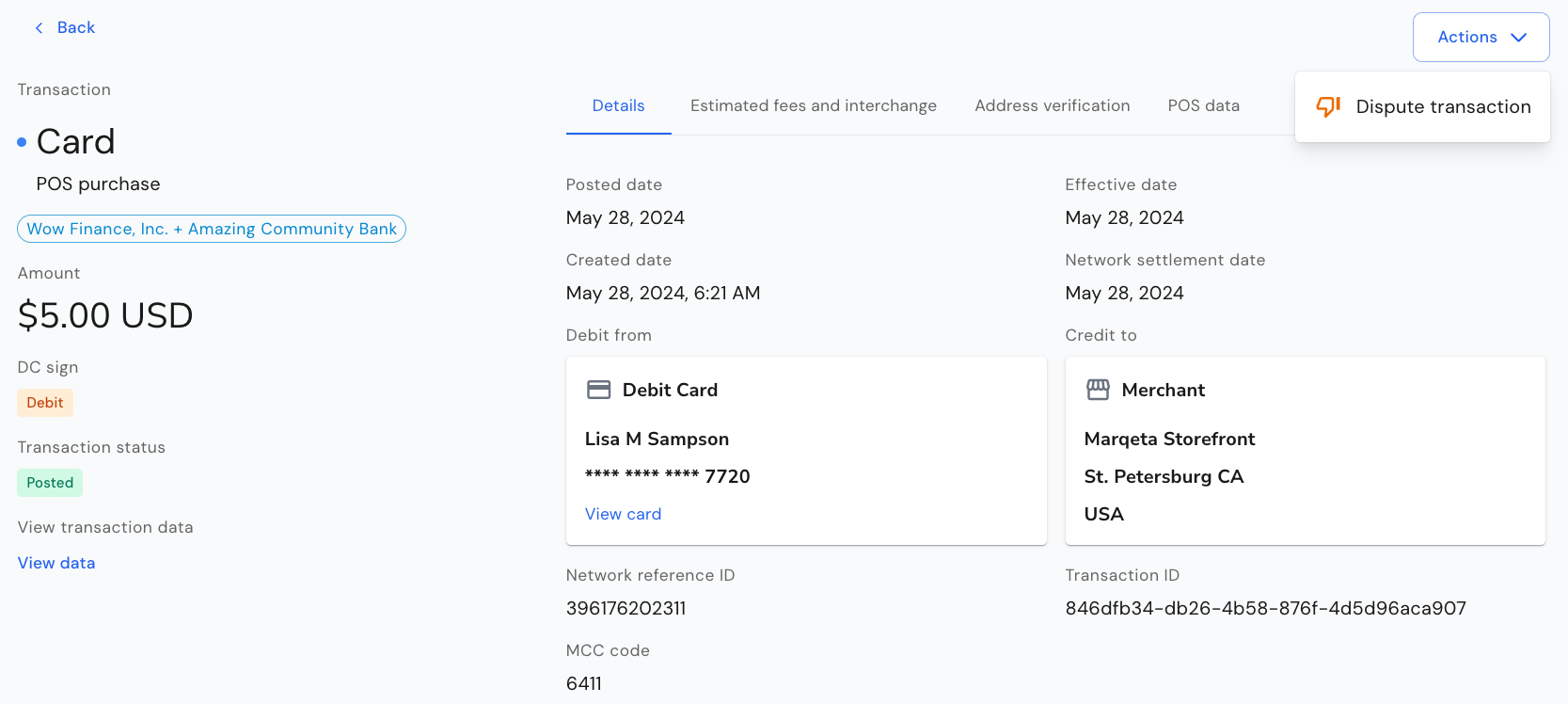

To dispute a cleared/posted transaction in the Synctera Console, go to Posted Transactions and Actions in the top right corner.

- Note:

- Information about the dispute, typically what the customer provides when submitting the dispute to the FinTech

- Dispute reason:

- The reason for the dispute - this reason may be overridden with a more appropriate/correct reason by the team reviewing the dispute

- Reasons include: ATM cash dispute, Card lost/stolen, Chip liability shift, Counterfeit goods, Credit not received, Defective goods or services, Dispute recurring transaction, Duplicate transaction, Fraudulent processing, Goods or services not provided, Late presentment, Paid by other means, Transaction amount differs, Transaction did not complete, Transaction not recognized, Unauthorized transaction

- Date reported:

- The date reported by customer is important for establishing the correct deadlines for provisional credit and investigation

- Disputed amount:

- This will be defaulted to the amount of the transaction being disputed on, in case of a partial dispute, to the remaining undisputed amount

What happens when the dispute is submitted?

- When the dispute is submitted, a dispute record is automatically created, and subsequently also the Synctera Dispute Case.

- Unless the transaction is disputed through Mastercard (enabled from November 2024), the case worker then needs to submit the case on Marqeta as Marqeta handles the communication with the networks’ dispute management systems for non-Mastercard disputes.

- Any status updates on Mastercard or Marqeta are automatically reflected in the Synctera Dispute Case.

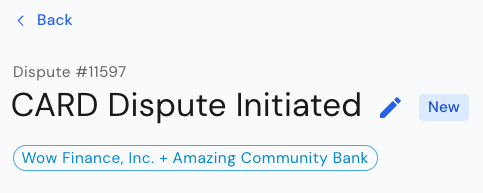

What’s displayed for Card Dispute cases

Case status

The case status is shown at the top of the Dispute case - to the right of the case description.

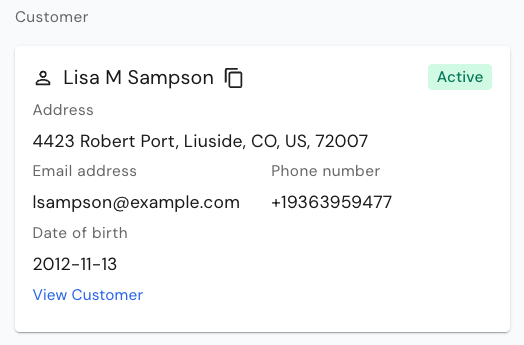

Customer

Shows information about the Customer to which the disputed transaction applies - click on the View Customer link to view full customer details:

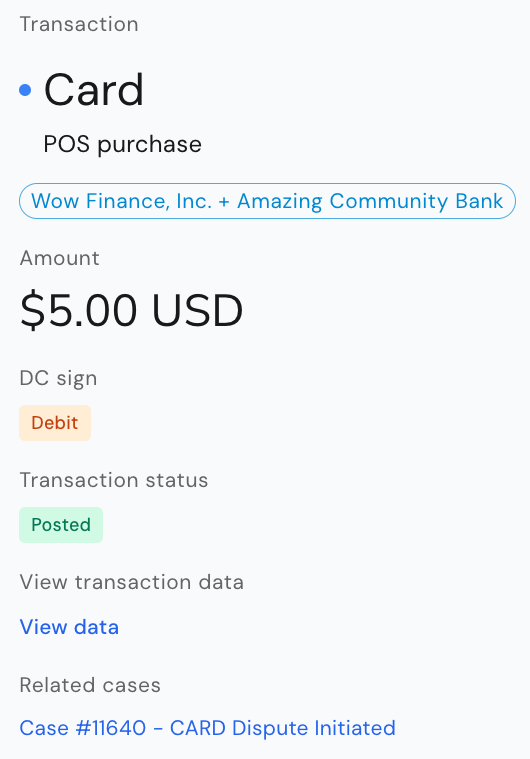

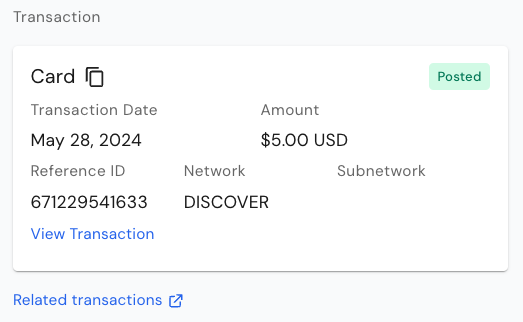

Transaction

Shows information about the Transaction being disputed - click on the View Transaction link to view full transaction details:

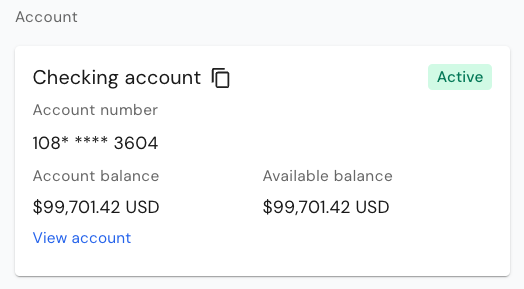

Account

Shows information about the Account to which the disputed transaction applies - click on the View Account link to view full account details:

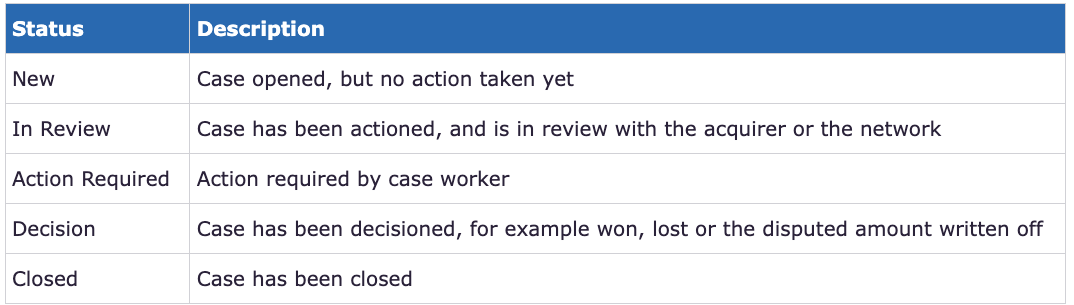

Lifecycle status, Decision and Credit status

Together, the Lifecycle status, Decision and Credit status tell you where the dispute is at.- The Lifecycle status tells you in which step in the dispute flow the dispute is

- The Decision tells you if a decision has been reached

- The Credit status tells you if a provisional credit or a final credit was posted or not

Note

The note that was entered when the case was submitted is shown below the Account information:

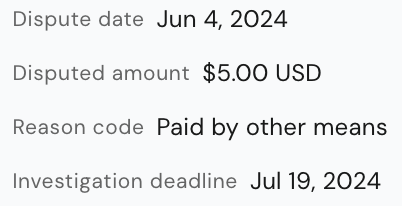

Submission details

Information about Disputed date, Disputed amount, Reason code and Investigation deadline, which is calculated automatically based on network timelines.

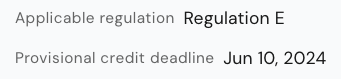

Applicable regulations and provisional credit requirements

Applicable regulation and provisional credit requirements are populated automatically based on the type of transaction (for example, consumer/commercial, debit/credit).

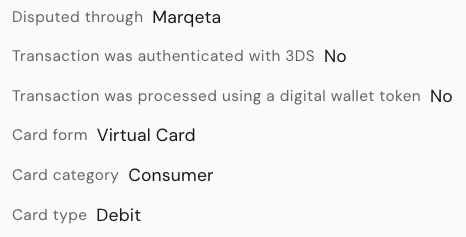

Other parameters impacting the dispute flow

There are various other parameters that impact the dispute flow and eligibility.- Disputed through: While the Synctera Dispute Case is not directly integrated with the networks dispute management systems, all transactions are disputed through Marqeta.

- 3DS authentication: If a transaction was authenticated through 3DS, it is not eligible for a chargeback with the network (i.e. will get rejected by the network).

- Digital wallet token transaction: If a transaction was processed using a digital wallet token, it is not eligible for a chargeback with the network (i.e. will get rejected by the network).

- Card form: It is of importance to know whether a physical or a virtual card was used for the transaction, as it may impact the decision.

- Card category: Rules and regulations are different for consumer and commercial cards.

- Card type: Rules and regulations are different for debit and credit cards.

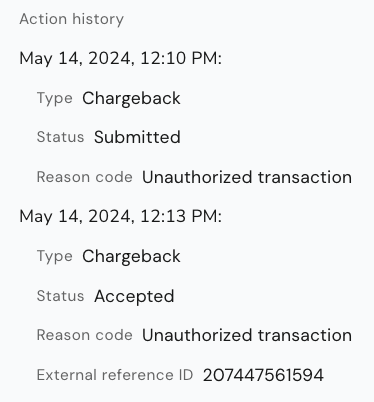

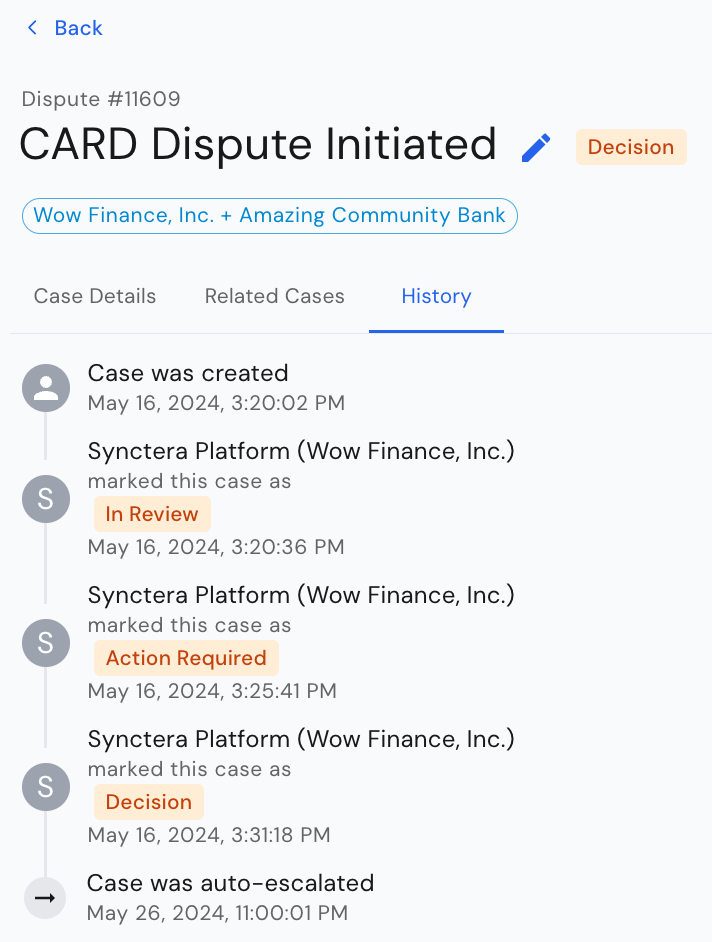

Action history

Shows all dispute lifecycle transitions/events:

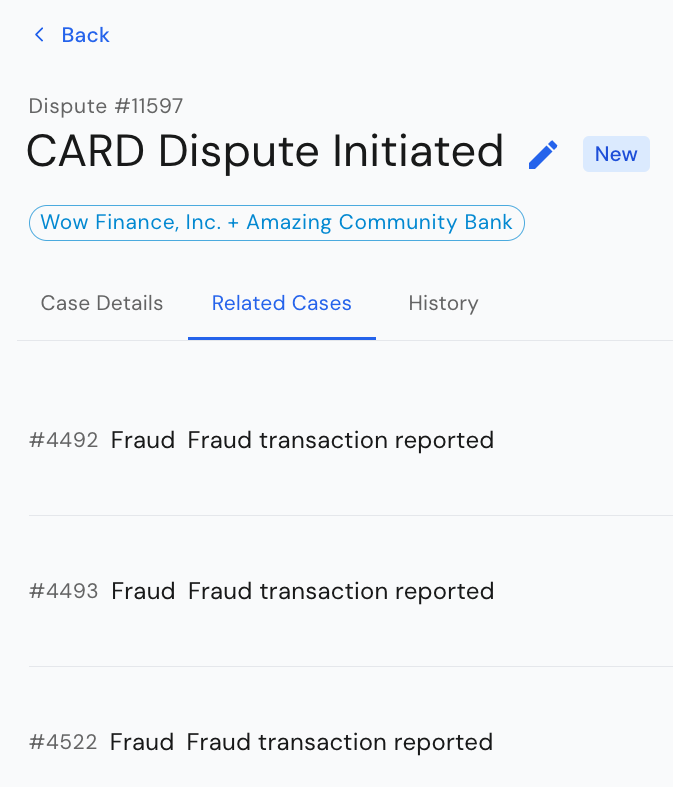

Related Cases

The second tab on the Dispute case shows Related cases, that is, other dispute cases opened for the same customer. This may help indicate whether a fraud pattern can be established for the customer.

History

The third tab on the Dispute case shows the case History, i.e. all the status transitions of the Synctera Dispute Case.

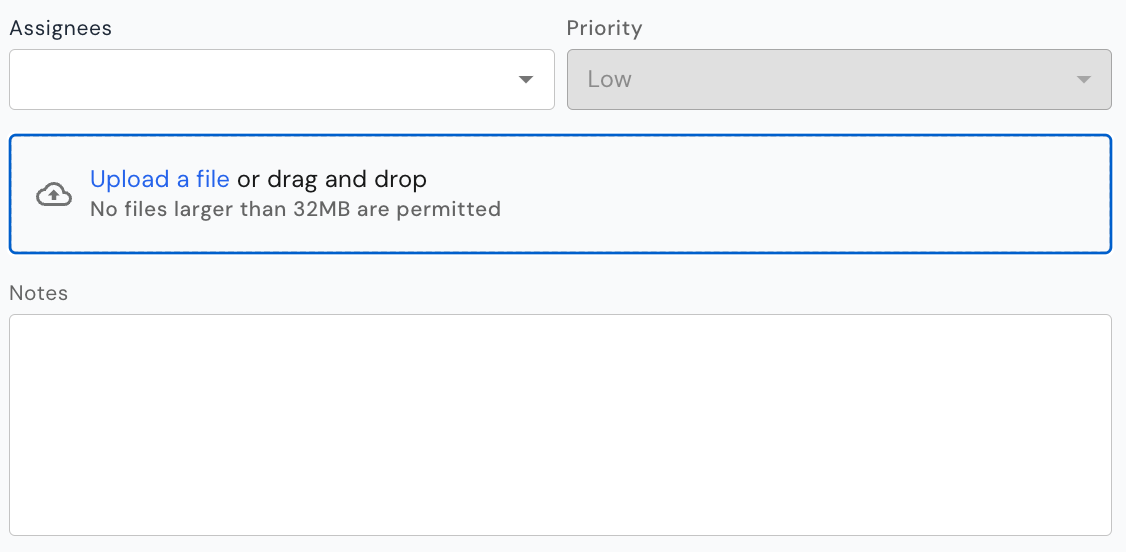

Case assignment and document upload

As for other case types, the Dispute case provides the ability to add an assignee and assign a priority to the case. In addition, documents can be uploaded to the case at any time, along with notes.

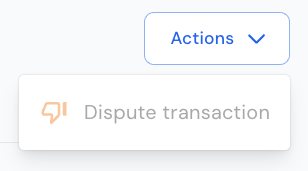

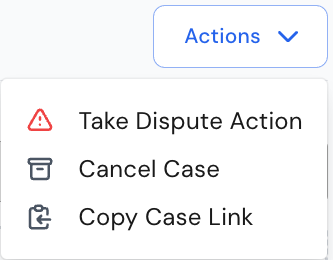

How to action a case

The system will automatically determine/display the case- and dispute-actions that are available based on:- The dispute status (lifecycle status / decision)

- Amount threshold - for card transactions, a dispute should not be submitted to the network if the disputed amount is below $25

Take Dispute Action

Current action limitations

- For disputes going through Mastercard, all dispute actions required to complete the dispute lifecycle are available in the Synctera Dispute Case.

- For disputes going through Marqeta (non-Mastercard disputes), the following limitations to dispute actions in the Synctera Dispute Case apply:

- No actions requiring direct communication with the card networks, such as initiating a chargeback (submitting to network), accepting a representment, etc., can be taken through the Synctera Dispute Case. These actions are handled through the Marqeta case, and then automatically reflected in the Synctera Dispute Case.

- Only actions that to not require communication with the card networks, such as posting of provisional credit, initiation of a write-off, etc., can be taken through the Synctera Dispute Case.

- Posting of provisional credits is done automatically, if required by regulations, within 10 business days for established accounts and within 20 business days for new accounts. However, there is an action, PROVISIONAL_CREDIT - CREATE, that can be used for immediate posting of the provisional credit.

- The WRITE_OFF - CREATE action initiates a write-off/posting of a final credit after 20 days - if a provisional credit exists at that point, it will automatically get reversed.

Cancel case

In the scenario where the customer would like to cancel a dispute, the case can be canceled as well.Close case

In the scenario where a decision has been reached (Decision = Won / Lost / Resolved) or case worker decides to deny the dispute, the case can be closed.